One To Three: The Story of Sequoia Capital's Split

Heard of the new kids on the VC block: Peak XV Partners and HongShan? …well, these cool kids aren’t exactly new.

Perhaps the names ‘Sequoia India & SEA’, and ‘Sequoia China’ ring a bell. Peak XV (“fifteen”) is an old name for Mt Everest, and Hong Shan transliterated to Chinese is “redwood”, a sequoia.

In this edition of The Conquest Communiqué, we explore Sequoia Capital’s splitting its partnerships and rebranding them into 3 firms — Sequoia Capital, Peak XV Partners, and HongShan — which happened earlier this week.

We discuss the details of the rejig, what could have caused this sudden move, and what the future effects of one of the largest VC firms in the world splitting could be.

The Split, and What Caused It

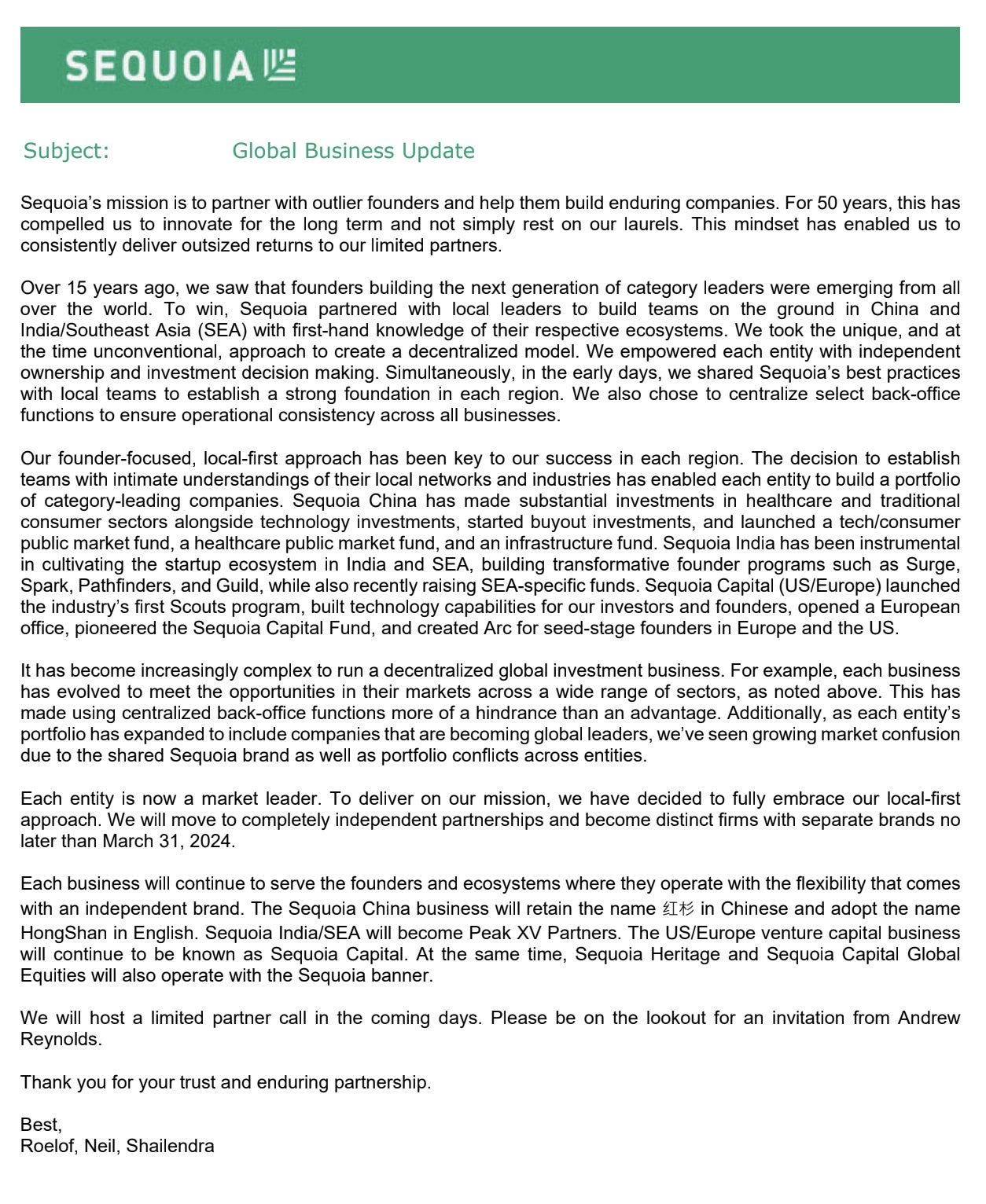

On Tuesday, Sequoia Capital released a letter to its LPs (limited partners). Having become a leader in their respective markets, its India and SEA business as well as the China business would become distinct firms with separate brands by March 2024.

In their official statements, the firms and their leaders cited the increasing complexities of running three partnerships with distinct strategies and markets as a prominent reason. With their growth, several back-office operations were beginning to become a hindrance.

Roelof Botha, Managing Partner of Sequoia Capital clarified that this was not a defeat:

“This isn’t a retreat saying, ‘white flag, we failed.’ It’s more of a victory in the sense that we have these fully independent businesses that can go even further.”

Another major cause, the leaders stated, was conflicts within their portfolio startups. For example, Stripe in the US and Airwallex in China – both portfolio companies of the respective arm – compete with a Razorpay company. Another U.S.-based Sequoia portfolio company complaining recently that an Indian-based rival backed by Sequoia’s team was publicising itself as the firm’s big bet in the sector, was a particularly “awkward” situation for Botha.

Such conflicts are ever more likely as the China and India Sequoia businesses look to expand their horizons beyond their domestic market sooner. Splitting into completely independent firms would free them of any more “awkward” scenarios.

Sequoia India and China were run independently earlier too. But profits from the franchises were still shared among the global partnership. This will end now, and the funds will not invest together going forward.

But when one of the largest VC firms on the planet undergoes such a major restructuring, it is not surprising that there are several other contributing factors.

China was already facing economic woes post the COVID-19 pandemic. The geopolitical tensions between the US and China have been worsening. The cherry on the top was TikTok (owned by Sequoia China’s portfolio company ByteDance) being banned for use by state employees in several US states over privacy violations.

The India and SEA arm of Sequoia, on the other hand, grappled with a few of its portfolio startups (BharatPe, GoMechanic, Zilingo…) hurting from fraud allegations and governance issues. Perhaps the mothership wanted to separate themselves and their funds more from any such instances out of fear of contamination. Especially after the whole FTX fiasco.

The whole thing, as is the case in the rest of the world today, has an AI undercurrent as well.

AI, the company believes, can lead to significant disruption, especially in developing Asian regions. Accordingly, the firm has evaluated each of its early-stage investments in the region to gauge the startups’ preparedness. Sequoia India & SEA, which has over 50 unicorns in its portfolio, also had a thing called “Learning Sundays," where they familiarised the startups’ teams with the latest developments in the field and potential impact on various sectors.

Over 75% of the new deals made by the arm in India & SEA were related to AI. Shailendra Singh, MD of the partnerships, referred once again to portfolio conflict: “If we got locked out of important companies in our region and couldn’t invest in them because of founder conflict in AI, that would be pretty debilitating.”

What does the future of venture capital hold?

As they complete the separation and move beyond, Botha hopes that Sequoia Capital, Peak XV Partners and HongShan will consider each other cousins through their shared heritage, even if they will no longer have any special relationship.

But here comes the interesting bit: no non-compete agreement was signed between the 3 firms! In this case, these are certainly going to be a competitive bunch of cousins, each relying on its strong brand and deep pockets to capitalise upon the next big thing. Something that Sequoia has always been known for, boasting early-investor status in Google, NVIDIA, YouTube, and a mind-boggling many others.

Talking specifically about Peak XV Partners, it will continue to invest Sequoia India & SEA’s last raised fund of $2.85 bn in the region. With a “dry powder” (uninvested capital) of $2.5 bn to deploy, the firm that already boasts of some of the biggest names of the Indian startup ecosystem (Razorpay, Ola, Cred, Byju’s, Unacademy, Mamaearth, Pine Labs…) will continue to be the one to watch out for.

Shailendra Singh is confident that their fundraising capabilities won’t be significantly altered: “...our brand is our relationships, and we feel our own brand is strong.” As each arm was previously independently managed too, raising capital from LPs shouldn’t be any more difficult than before. The separate firms, with their specialised focus and deep understanding of local markets, may align more closely with the investment preferences of some LPs looking to gain exposure to these specific markets through the expertise of the newly formed entities.

It would not come as a surprise to see other large VC firms with significant international presence follow in Sequoia’s footsteps in the near future. The thought does seem promising on the whole. As Anand Lunia, founder partner at early-stage fund India Quotient, put it:

“With the extra power will come extra responsibility and I feel they will continue to be drivers of the ecosystem… This split is in line with what's going on in many other fund brands, but it has only been better for Indian startups.”