How Venture Capital Ventured into India

From seed capital to the Silicon Valley influence, the story of how VC entered India

India has over 110 unicorns today, with dozens more in the making. Supporting the ecosystem, the Indian Venture Capital Association (IVCA), India’s apex association for Venture Capital and Private Equity firms, has 330 members, managing a massive $260 billion in assets.

However, India from the early-1970s paints a completely different picture: there were neither any startups to boast of, nor institutions willing to fund you if you wanted to build one.

The three-decade journey of VC’s entry to India from the late 1970s to the early 21st century has been nothing short of remarkable. In this edition of The Conquest Communiqué, let’s take a deep dive into this fascinating story.

IDBI sets the Stage

The year of 1976 saw a breakthrough in startup-financing. The Industrial Development Bank of India (IDBI), originally an RBI subsidiary, was made the Government of India’s principal institution for managing industry-financing.

Just a few months later in 1976, the IDBI launched the Seed Capital Assistance Scheme: a scheme where the government would cover a partial cost of your startup if you were a technologically-skilled first-generation entrepreneur.

Before 1976, all financing institutions had been created to promote relatively large industries, leaving practically no avenues to raise money as a new entrepreneur or technologist. However, the seed capital scheme was focussed on new technology companies. The scheme provided financial assistance in the form of soft loans, equity deals, or a mix of both.

Over the next decade, this scheme helped more than 300 projects, disbursing over ₹9 crores, which is huge when adjusted for the value of the Indian Rupee in that time. Hence, the Seed Capital Assistance Scheme laid the groundwork for Venture Capital in India by introducing the idea of funding startups.

Startups get a Dedicated Fund

In the seed capital scheme, it was IDBI’s money that was being invested into the startups; there was no separate fund. This continued for a decade before the Union Budget of 1986–87 proposed a separate Venture Capital Fund (VCF) for the scheme, marking a major milestone in the journey.

Since the initial focus was on funding technology companies, the first VCF was actually a Technology Development Fund (TDF), meaning that only new technology startups would receive funding. Initially, ₹10 crores were added to this from government revenue.

However, it would be unsustainable to keep funding startups from public funds because of the high risk associated with investing in startups, which could potentially cause losses to the government, negatively impacting all government initiatives. So where would money for the fund come from?

In the budget of 1986–87, Finance Minister Mr. Narayan Dutt Tiwari introduced the Research and Development Cess on Indian companies. Indian companies, in those days, had to frequently import technology for use in their products. On all such imports, the government levied a 5% cess and used this money for the VCF.

This therefore marked the formalisation of Indian VC, because for the first time, there was a dedicated fund for investing in startups, along with a sustainable source of capital for the fund: the import cess.

Private Firms fill in the Gaps

As evident from the 1976 seed capital scheme as well as the 1986–87 Union Budget, the need and importance of financing early-stage ventures had been realised by the government. This was further expressed by the Finance Minister in the 1988–89 Union Budget speech:

We have one of the largest pools of scientific and technical manpower. Yet many of our young and new entrepreneurs find it difficult to raise equity capital because of the risks involved. Allowing venture capital companies to undertake high-risk equity financing in anticipation of future capital gains can solve this problem.

Incentivising private firms to invest in startups in 1989 was a tough task; not only because it was a practice that was alien to contemporary India, but also because hardly 3 years had passed since the stock market crash of 1986, which had hugely affected investor confidence.

The solution the government came up with was capital gains concession. Basically, on every rupee you earn in profit from an investment, the government levies a capital gains tax. This capital gains tax is typically higher for corporations than it is for individuals.

The idea was to offer investment corporations a lower capital gains tax if their profit was from investment in a startup instead of a large company. This was implemented 1990 onwards.

This groundbreaking idea led to several private VC firms mushrooming in India over the next few years. By 1999, the number of VC firms had increased to more than 20 from just around 8 at the start of the decade.

Silicon Valley delivers the Final Stroke

The first few years following the capital gains concession saw turbulent growth for Indian VC. This is because since the sector was nascent, most firms had poor management teams, stalling their growth.

Additionally, the regulatory environment was uncertain, because the government, owing to its heavy initial focus on technology startups, hadn’t opened up all areas for early-stage investment, leading to several industrial sectors being ineligible for VC investment.

However, these issues were resolved over the next few years, as subsequent government policies opened up more sectors for investment and firms started coming of age, their management teams improving.

Then came the Silicon Valley boom: a blessing in disguise.

Santa Clara Valley, or Silicon Valley, saw a huge boom in the number of successful companies in the 1990s; and many of these were founded by Indians. This led to VC funds from across the world being drawn to the Indian startup ecosystem, expecting a replication of Indians’ success abroad.

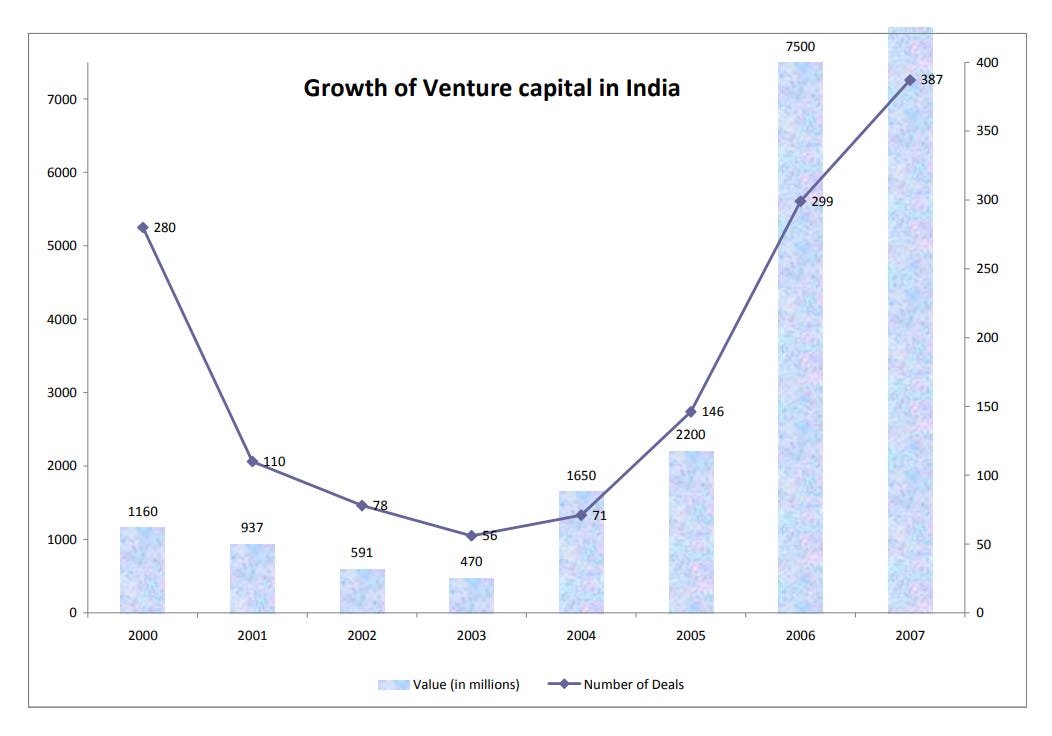

The result? In 1999, over 80% of VC money invested in India was from foreign firms. This kickstarted innovation in multiple sectors at a time the internet and personal-computer sectors were booming. For example, US-based Indigo Monsoon Group (IMG) led an angel-investment into Indiaplaza, launched in 1999 as Fabmart.com— India’s first online departmental store.

As the years passed, VC firms began springing up inside India to benefit from India’s expected startup boom. In 2002, India became the second most active venture capital market among 10 major Asia-Pacific economies in terms of the total investment.

Today, the Indian VC network has evolved into a full-blown ecosystem. Venture Capitalists are no longer mere cash machines for startups; they provide an entire environment of support: including mentorship, assistance in cracking better deals, and access to their extensive networks in the industry.

VCs are also becoming increasingly collaborative, actively participating in startup accelerator programs and working closely with the founders themselves during decision-making. This evolution has enabled Indian VC giants including the likes of Blume Ventures, Kalaari Capital and Elevation Capital among others to stand head-to-head with global giants.

India’s journey from having no VCs at all to now having sector-specific VCs and an extensive micro-VC network has been remarkable. Today, the number of rapidly growing VC firms and other investors in the Indian startup ecosystem shows their conviction in India’s growth story. This reaffirms India’s position as the next global leader.

| A guest post by

|